How to Transfer Your Income Into Your Trust: A Complete Guide

Creating a revocable living trust is only the first step in protecting your family from probate court. The critical second step—one that 50-80% of people with trusts never complete—is actually transferring your assets and income streams into that trust.

This guide will walk you through exactly how to transfer your income into your revocable living trust, what types of income need to be addressed, and why this process is absolutely critical for your family's financial security.

Understanding What Legally Qualifies as Income

Before you can protect your income, you need to understand what the law considers "income." The IRS defines income broadly, and all of these sources should be addressed in your estate planning:

- Employment income: Salaries, wages, bonuses, commissions, and tips

- Self-employment income: Business profits, contract work, and freelance earnings

- Investment income: Interest from bank accounts, corporate bonds, and dividend-paying stocks

- Capital gains: Profits from selling stocks, cryptocurrency, or real estate

- Rental income: Revenue from investment properties

- Royalties: Ongoing payments from intellectual property, patents, or mineral rights

- Government benefits: Social Security benefits, unemployment compensation, and VA disability compensation or pension

- Insurance proceeds: Claim payments (typically not taxable, but still part of your estate. This is the one exception—not typically considered income)

- Gambling winnings: Casino winnings, lottery prizes, and other gaming proceeds

Each of these income types flows into your bank accounts. And if those bank accounts aren't properly titled in your trust when you die, your family will face the probate nightmare you were trying to avoid.

The Probate Consequence: What Happens If Your Income Isn't in Your Trust

Here's the harsh reality: even if you have a notarized will, if your bank accounts (where all this income flows) aren't properly connected to your trust, your family will still suffer through probate court.

The statistics paint a grim picture:

- Average probate duration: 20 months nationally, with California estates averaging 9-18 months and complex estates taking up to 2 years or more

- Average probate costs: 5-10% of the total estate value. For a $500,000 estate, expect $25,000-$50,000 in fees. For a $750,000 estate, costs can reach $37,500-$75,000

- Public exposure: 100% of probate proceedings become public record, searchable online by anyone—including predatory attorneys, scammers, and estranged relatives

According to Trust & Will's 2024 Probate Study, a staggering 56% of Americans have no idea what probate actually costs, with many believing it will cost $1,000 or less. Only 2% of survey respondents understood that probate takes an average of 20 months to complete.

These aren't just statistics—they represent real families sitting in courtrooms during the worst season of their lives, watching their inheritance dwindle away in legal fees.

How to Actually Transfer Your Income Streams Into Your Trust

The good news is that the process of protecting your income is surprisingly straightforward. There are two primary methods, and most people will use one or both depending on their bank's policies.

Method #1: Account Retitling (The Preferred Method)

The cleanest solution is to ask your bank to retitle your existing bank account from your personal name into your trust's name.

Here's the exact format you need:

[Your Name] trustee of the [Your Trust Name] revocable trust, dated [Date Trust Was Created]

For example: Bobby McGee trustee of the Bobby McGee Family revocable trust, dated December 15, 2026

Critical requirements:

- You must include your name as the trustee

- You must include the exact name of your trust

- You must include the date your trust was opened

If you fail to include any of these three elements, your bank account is not properly owned by your trust, and you will run into serious problems.

What to bring to your bank:

- Your complete trust documentation

- A Certification of Trust (a shorter document that proves your trust exists)

- Your government-issued identification

Most major banks (Chase, Bank of America, Wells Fargo, U.S. Bank, PNC, Truist) and credit unions will happily retitle your existing account. Approximately 70-90% of branches will complete this process if you ask confidently and come prepared with proper documentation.

Why this method is superior:

- Zero disruption to your financial life

- Same account number, debit card, and online banking login

- All automatic payments continue without interruption

- All direct deposits continue to the same account

- Complete probate protection upon your death

Method #2: Opening a New Trust Account (When Retitling Isn't Available)

If your bank refuses to retitle your existing account, they will likely recommend opening a new bank account with the trust as the owner from day one.

This method is more of a hassle because you'll need to:

- Transfer all funds from your old account to the new trust account

- Update every automatic payment (utilities, mortgage, subscriptions, insurance)

- Notify everyone who pays you via direct deposit (employers, clients, pension providers, Social Security Administration)

- Update payment information on all online platforms

- Close your old personal account once everything has been transferred

While more cumbersome, this method is just as legally sound and provides the same probate protection as retitling. For most people, this represents 10-20+ hours of administrative work, but it's a one-time investment that protects your family from months of probate proceedings.

Special Considerations for Government Benefits

There's an important nuance when it comes to certain government benefit programs.

The three income sources that may require special handling:

- Social Security retirement or disability benefits

- Unemployment compensation

- VA disability compensation or pension

The workaround solution:

If you encounter resistance from any government agency or employer who insists on an exact name match with no trust language:

- Open a separate personal bank account in your exact legal name (no trust language)

- Set up direct deposit from the government agency or employer into this personal account

- Transfer funds from your personal account into your trust's account on a regular schedule

With modern online banking platforms like Mercury, Ally, or Capital One 360, you can open a personal account in under 60 seconds and set up automatic transfers to move funds into your trust's account immediately upon receipt.

This two-step process ensures you receive your benefits without complications while still getting the funds into your trust for probate protection.

Understanding the Tax Implications

One of the most common concerns people have is: "If my income goes into a trust, how does that affect my taxes?"

The answer is simple and reassuring: a revocable living trust has zero impact on your income taxes during your lifetime.

Here's why:

The IRS treats revocable living trusts as "grantor trusts" under Internal Revenue Code sections 671-679. This means the trust is completely transparent for tax purposes—the IRS essentially pretends it doesn't exist.

What this means in practice:

- All income your trust receives is counted as income you personally receive

- You report everything on your personal Form 1040 tax return

- You are 100% responsible for all income tax and FICA tax (Social Security and Medicare taxes)

- Your tax identification number remains your Social Security number—you don't need a separate EIN for your revocable trust while you are still alive.

- You typically don't file a separate trust tax return (Form 1041) while you're alive and the trust is revocable

Think of it this way: your revocable living trust is treated exactly like an LLC for tax purposes. It's a pass-through entity. The income flows through to your personal return as if the trust doesn't exist.

This tax treatment only changes after your death, when the trust becomes irrevocable. At that point, your successor trustee may need to file Form 1041 and obtain a separate tax identification number. But during your lifetime, there's no additional tax complexity whatsoever.

Understanding Your Three Roles in the Trust

When you create a revocable living trust, you typically serve in three different roles simultaneously. Understanding these roles helps clarify why the tax treatment is so simple:

- Grantor (or Settlor/Trustor): You're the person who created the trust and transferred assets into it

- Trustee: You're the person who manages the trust assets and makes all decisions

- Beneficiary: You're the person who benefits from the trust assets during your lifetime

Because you occupy all three roles, you maintain complete control over your money. You can spend it, invest it, give it away, or do anything else you want with it—exactly as if the trust didn't exist.

The only time the trust's ownership matters is when you die. At that moment, your successor trustee (the person you named to take over) steps into the trustee role and distributes your assets according to your instructions—all without probate court involvement.

Why This Process Matters: The Three Catastrophic Consequences of Failing to Fund Your Trust

Every estate planning attorney has heard the same heartbreaking story: "My parents spent $3,000 creating a beautiful trust, but when they died, we still went through probate because they never funded it."

Don't let this be your family's story. Here are the three devastating consequences they'll face if you don't complete this process:

Consequence #1: The Money Grab

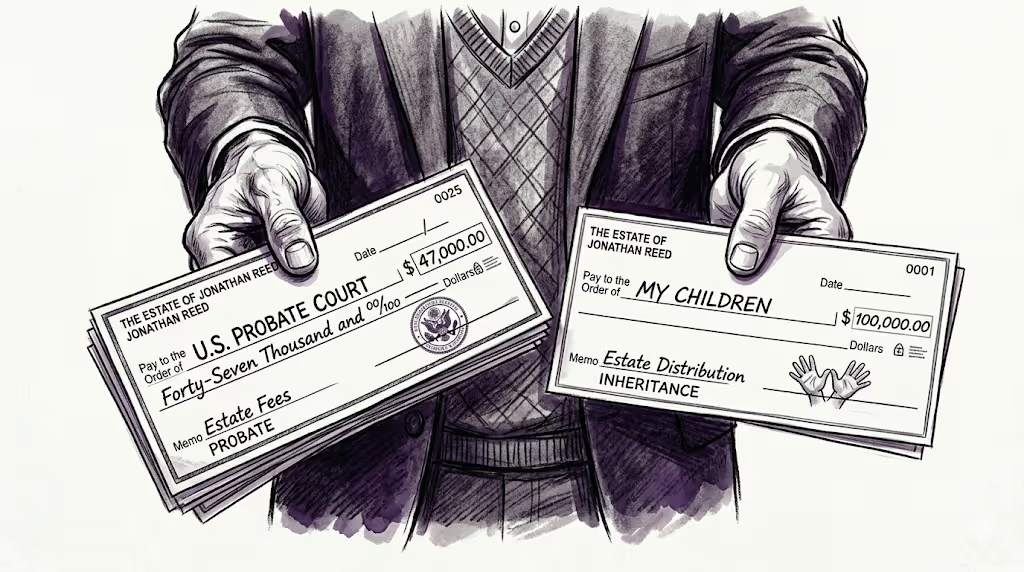

Any money in bank accounts not properly titled in your trust will go through probate court. The court system and attorneys will take 5-10% off the top to pay for court costs and legal fees.

On a $500,000 estate, that's $25,000-$50,000 gone—money that should have gone to your children or grandchildren but instead goes to paying probate lawyers and court administrators.

In California, the numbers are even worse. Due to statutory fee schedules, both the attorney and the executor each receive $13,000 on a $500,000 estate—that's $26,000 in fees before court costs and other expenses.

Consequence #2: The Waiting Game

Your family will sit through 6-24 months of probate proceedings during one of the worst seasons of their lives. They've just lost you, and instead of grieving and healing, they're attending court hearings, filling out endless paperwork, and waiting for a judge to give them permission to access money that should have been immediately available.

According to recent data, the average probate in California takes 9-18 months for straightforward estates. Complex estates or those with disputes can drag on for 2-3 years or longer.

During this entire period, your family may struggle to pay final expenses, settle debts, or access inheritances they desperately need.

Consequence #3: The Public Exposure

Everything becomes public record. Your assets, your debts, your beneficiaries, their addresses, the amounts they're receiving—all of it becomes searchable online by anyone with internet access.

This public exposure invites:

- Predatory attorneys looking for estates to file claims against

- Scammers targeting your grieving family members

- Estranged relatives appearing to contest the will

- Creditors (both legitimate and fraudulent) making claims against the estate

- Identity thieves harvesting personal information

The emotional toll of dealing with these vultures during an already difficult time cannot be overstated. And all of it could have been avoided by properly funding your trust.

The Simple Action Steps

Don't let your trust become another unfunded document gathering dust in a filing cabinet. Here's your action plan:

- This week: Schedule appointments with every bank where you have checking or savings accounts

- Before each appointment: Gather your trust documentation, certification of trust, and ID

- At the appointment: Request account retitling using the exact format: [Your Name] trustee of the [Trust Name] revocable trust, dated [Date]

- If retitling isn't available: Open a new bank account owned by your trust and begin the process of transferring automatic payments and direct deposits

- For government benefits: If you encounter resistance, set up a separate personal account and create automatic transfers to your trust account

- Document everything: Keep copies of all retitled accounts and new account paperwork for your successor trustee

Common Questions About Income and Trust Funding

Do I need to retitle my retirement accounts?

No. IRAs, 401(k)s, and other retirement accounts should NOT be retitled into your trust. Instead, you should name your trust as the beneficiary of these accounts. Retitling retirement accounts into a trust can trigger immediate income taxes and penalties.

What about business income from an LLC or S-corporation?

Business income flows through the business entity to you personally, then into your bank accounts. As long as your bank accounts are properly titled in your trust, the income is protected. The LLC or S-corp itself may or may not need to be owned by your trust, depending on your specific situation and state laws.

What if I open new bank accounts in the future?

Any new accounts you open should be opened in the name of your trust from day one. Use the same naming format: [Your Name] trustee of the [Trust Name] revocable trust, dated [Date]. Most banks will let you open accounts in your trust's name as easily as opening accounts in your personal name.

Can I still write checks and use my debit card?

Absolutely. When your account is retitled, you maintain complete access and control. Your checks and debit cards will work exactly as before. Some banks may issue new checks with the updated account name, but many allow you to continue using your existing checks.

What about credit card rewards or cash back that get deposited?

These are considered income and will be deposited into your bank account. As long as that bank account is titled in your trust, the rewards are protected.

The Bottom Line

Creating a revocable living trust without funding it is like buying a safe and leaving all your valuables sitting on the kitchen counter. The protection exists, but you're not using it.

According to estate planning professionals, 50-80% of revocable living trusts are never properly funded. This means that despite spending thousands of dollars on trust creation, the majority of families still end up in probate court because the critical funding step was never completed.

Don't become part of this statistic.

Take action this week. Schedule those bank appointments. Get your accounts retitled. Protect your family from the probate nightmare that robs them of time, money, and peace of mind during their darkest hours.

Your trust is only as good as the assets it contains. Make sure your income streams are properly protected.

Need Help With Trust Funding?

If you're feeling overwhelmed by the process of funding your trust or want professional guidance to ensure everything is done correctly, we're here to help. Book a complimentary 15-minute consultation to discuss your specific situation and create a customized funding plan.

The 15 minutes you invest now could save your family 15 months of probate court and $15,000+ in unnecessary fees.

Need help? Apply for a 30 minute consultation here.

Disclaimer: This article provides educational information about estate planning and asset protection strategies. It is not legal, tax, or financial advice. Every situation is unique and requires personalized guidance from qualified professionals. Laws vary by state and change frequently. Consult with licensed attorneys, CPAs, and financial advisors before implementing any strategies discussed.

Recommended articles

Essential guides to protect and preserve your family's wealth

Stay informed about wealth protection

Get expert strategies and insights delivered to your inbox weekly