The Complete Guide: 9 Categories of Assets You Must Put in Your Trust

What should you put into your trust? Here's everything you need to know about protecting your family's future.

When it comes to estate planning, one of the most common questions people ask is: "What exactly should I put into my trust?" It's a critical question—because the answer determines whether your loved ones will smoothly receive their inheritance or spend months (even years) battling through probate court.

The statistics are sobering. Currently, 55% of Americans have no estate plan at all and only 24% have a will while just 11% have a trust. Even more concerning, the average probate court process costs between 5-10% of assets and can take anywhere from 6 months to 2 years to complete.

But here's what most people don't realize: having a trust isn't enough. You must properly fund your trust by transferring assets into it. Otherwise, those assets will still go through probate, defeating the entire purpose of creating a trust in the first place.

Let's explore the nine essential categories of assets that should be in your revocable living trust—and why each one matters for protecting your family's future.

Understanding Revocable vs. Irrevocable Trusts

Before we dive into what goes into your trust, it's important to understand a key concept: While you're alive, your revocable living trust gives you complete control over all assets within it. You can buy, sell, trade, or modify anything you want.

The magic happens when you pass away—at that point, the trust typically becomes irrevocable, which means the assets are protected and distributed according to your specific instructions without government interference or probate court involvement.

This flexibility during your lifetime combined with protection after your death is what makes revocable living trusts such powerful estate planning tools.

Category 1: Real Property

Real property means land and anything permanently attached to it. Real property represents some of the most valuable assets most families own, and it's absolutely critical to transfer these into your trust.

What qualifies as real property:

- Primary residences and vacation homes

- Undeveloped land and acreage

- Mineral rights (the right to extract valuable materials from land)

- Commercial properties like apartment complexes, office buildings, or retail spaces

- Timeshares and fractional property ownership

- Agricultural land and farms

Real property is particularly vulnerable to probate because it's often the most valuable single asset in an estate. Without proper trust funding, your family may face significant delays in accessing or selling property while it works through the court system.

Real-world example: One client we are working with in Kentucky owns 750 acres with coal mining rights. By placing both the land and the mineral rights into his trust, he ensures that his family can continue benefiting from lease income without interruption when he passes.

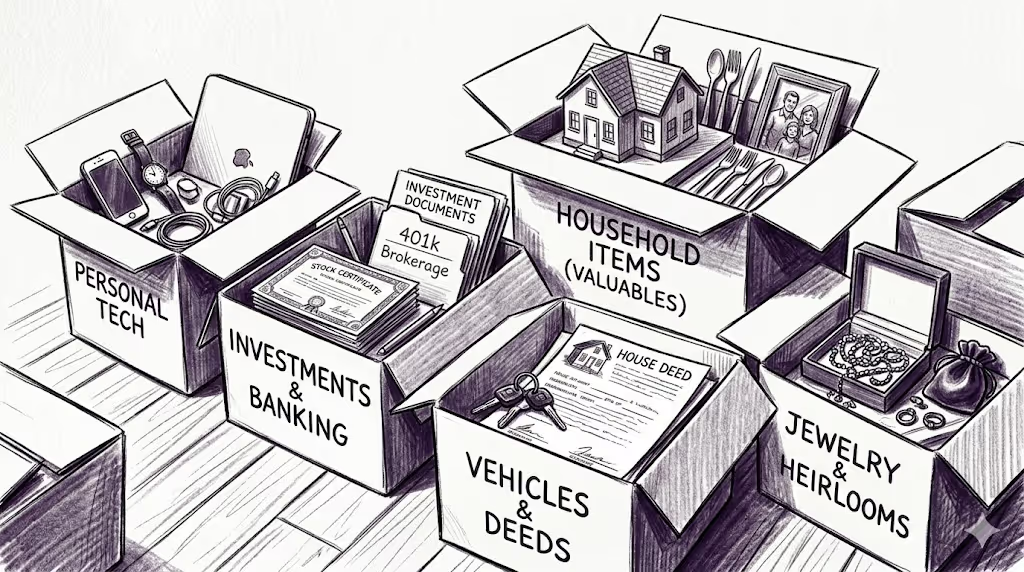

Category 2: Personal Property

Personal property includes tangible items you own that are not real property—and contrary to popular belief, these items absolutely need to be included in your trust.

Examples of personal property:

- Vehicles (cars, trucks, motorcycles, boats, RVs)

- Jewelry and watches

- Furniture and household items

- Firearms and weapons collections

- Art, antiques, and collectibles

- Safe deposit boxes and their contents

Many people mistakenly believe: "It's not a big deal when I die—just give this to Bobby and that to Lucy. I included it in my will, so we're good."

Unfortunately, that's not how it works. Unless personal property is specifically transferred into your trust through a process called "bequeathing," it will go through probate—even if you have a will.

How to transfer personal property: Since most personal property doesn't have formal titles, you transfer it to your trust by creating a detailed assignment document that lists specific items and designates beneficiaries for each one.

Category 3: Intangible Property

Intangible property represents assets that hold value but cannot be physically touched. In our digital age, this category has become increasingly important—and frequently overlooked.

Types of intangible property:

- Patents and pending patent applications

- Copyrights and publishing rights

- Trademarks and service marks

- Business goodwill and brand authority

- Domain names and websites

- Social media accounts with commercial value

- Email lists and customer databases

The test for whether something qualifies as intangible property is simple: Would someone pay money for it? If the answer is yes, it belongs in your trust.

Example: If you've built a website that generates revenue or a brand that has recognition and value, these assets can be transferred to your beneficiaries through your trust—preserving the business value you've created.

Category 4: Income and Financial Assets

This broad category encompasses various streams of income and financial holdings that generate ongoing value.

What to include:

- Stocks, bonds, and securities

- Mutual funds and index funds

- Royalties from books, music, or patents

- Rental income from investment properties

- Structured settlement payments

- Insurance claim proceeds

- Certificates of deposit (CDs)

- Money market accounts

- Cash holdings (whether in banks or at home)

- Health Savings Accounts (HSAs)

- Healthcare Flexible Spending Accounts (HFSAs)

Important distinction: Note that rental property itself is "real property" (Category 1), but the income generated from that property is a financial asset that should also be titled to your trust.

Category 5: Retirement Accounts

Retirement accounts require special handling in estate planning, but they're too important to overlook.

Types of retirement accounts:

- 401(k) plans

- Traditional IRAs and Roth IRAs

- 403(b) plans

- Pension plans and defined benefit plans

- Employee Stock Ownership Plans (ESOPs)

- SEP IRAs and SIMPLE IRAs

- Keogh plans

Special consideration: With retirement accounts, you typically name your trust as the beneficiary rather than retitling the account itself. This approach preserves the tax-advantaged status of the account while ensuring the funds are distributed according to your trust's instructions.

Over the next three decades, American retirees plan to transfer more than $36 trillion to various beneficiaries. Proper planning for retirement accounts is essential to maximizing what your family receives.

A critical mindset shift: Young, healthy people often think estate planning isn't urgent. The harsh reality is that you never know when your last day will be. Don't leave a legacy where the last thing your family remembers is being forced into probate court for six months to two years because you didn't prioritize setting up your estate plan.

Category 6: Insurance and Annuities

Life insurance and annuities deserve special attention because of their potential to either build or destroy your legacy—depending on how you structure them.

What to include:

- Life insurance policies with death benefits

- Whole life and universal life policies with cash value

- Policy loans against insurance

- Qualified and non-qualified annuities

- Long-term care insurance

- Disability insurance with payable benefits

The Smart Way to Handle Life Insurance

Here's a scenario that plays out far too often: A parent has a $1 million life insurance policy with their child named as the direct beneficiary. When they die, that child receives the entire million dollars in one lump sum.

The problem: If your child has never managed large sums of money before, research shows that the vast majority of windfall recipients spend it all within one to two years—and many end up miserable, realizing the devastating financial mistakes they've made.

Giving someone an enormous amount of money can actually be one of the worst things you can do for them if they're not prepared to handle it responsibly.

The solution: Spendthrift provisions

By making your trust the beneficiary of your life insurance policy, you can include "spendthrift provisions" that control how and when the money is distributed.

Example: Instead of receiving $1 million at once, your trust could be structured to pay your child $10,000 per month. This provides financial security while preventing the reckless spending that often accompanies sudden wealth.

Real-world case study: A recent client (we'll call her Lucy) has two adult children in their fifties. Her daughter and son-in-law struggle with alcoholism, creating an unstable environment for their children. Lucy does not want her daughter receiving a large inheritance while battling addiction.

The solution: Lucy can structure her trust so that her daughter cannot receive her inheritance until she has tested clean for alcohol every month for two consecutive years. Then, the funds will be distributed in controlled portions over time.

This approach puts powerful incentive in place for positive change while protecting the inheritance from being squandered during active addiction.

That's how customizable and protective a well-designed trust can be.

Category 7: Business Interests

If you own any part of a business, those interests need protection through your trust.

Business assets to include:

- LLC membership units

- C-Corporation shares (check the by laws and agreements)

- Partnership interests

- Professional practice ownership (medical, legal, accounting, etc., but you have to be licnesed in this practice).

- Sole proprietorship assets

- Buy-sell agreements (check agreements)

Transferring business interests to your trust accomplishes multiple goals: It ensures smooth succession planning, avoids business disruption during probate, and protects your ownership from being tied up in court while your family waits for estate settlement.

Important note: You can still operate and control your business exactly as before—the trust ownership doesn't change your day-to-day management. But when you pass away, the transition happens seamlessly according to your instructions rather than through months of probate proceedings.

Category 8: Digital Assets and Online Holdings

In our digital age, this category is rapidly growing in importance—yet it's the most frequently overlooked in traditional estate planning.

Digital assets to consider:

- Cryptocurrency (Bitcoin, Ethereum, and other digital currencies) (usually allowable when not stored on the exchange)

- Cold storage wallets and hot wallets

- NFTs (non-fungible tokens) (if self-owned)

- Online business assets and e-commerce stores

- Digital intellectual property

- Cloud storage accounts with valuable data

- Online investment accounts

- Digital photos and videos with sentimental or commercial value

Cryptocurrency and digital assets present unique challenges because they can be nearly impossible to access without proper documentation. Make sure your trust includes detailed information about how to access these assets, including (stored securely) any necessary passwords, recovery phrases, or access keys.

The Devastating Cost of Incomplete Planning: A Real Case Study

Let me share a real situation that illustrates why this matters so much.

Recently, we spoke with an 80-year-old woman (we'll call her Lucy) whose husband had recently passed away. He thought he had done everything right—he had a will that specified who should get what.

But he never created a trust.

Because all his assets had to go through probate court, do you know how much his estate transferred to the government in fees and costs?

$12,000.

That's $12,000 that could have gone to their children and grandchildren—money that instead went to court costs, attorney fees, and government processing simply because he didn't properly structure his estate plan.

This is money that was essentially wasted. It provided zero value to the family. It was simply a tax on poor planning.

And beyond the financial cost, consider the emotional toll: Lucy's family spent months navigating the probate system during their time of grief, dealing with paperwork, court appearances, and delays when they should have been healing and remembering their loved one.

35% of American adults say they or someone they know have experienced family disputes because they lacked proper estate planning documents. The emotional damage can far exceed the financial costs.

The Government's Plan for Your Estate

Here's a truth many people don't want to face: If you don't set up a plan for your estate, the government has a plan for you.

That plan will cost you money, cost you time, and cost you privacy.

Three costs of probate:

- Money: Probate expenses typically cost between 5-10% of an estate's total value, including personal representative fees, attorney fees, accounting fees, appraisal and business valuation fees, bond fees, and various court costs.

- Time: The average modest estate can take 6 months to 2 years to work through the probate process. More complex estates or those with disputes can take significantly longer.

- Privacy: Probate proceedings are public record. This means anyone can access information about what you owned, what you owed, and who received what. High-profile examples include Michael Jackson's estate (valued at approximately $2 billion after his death despite initial debts) and Prince's estate (estimated at $156 million), both of which became public knowledge due to probate.

Common Misconceptions About Estate Planning

Myth #1: "I don't have enough assets to need a trust"

40% of respondents feel they don't have enough assets to justify creating estate planning documents. This is one of the most dangerous misconceptions. Even modest estates face probate, and the percentage costs can be even more devastating for smaller estates.

Myth #2: "A will is enough to avoid probate"

50% of Americans who have a basic will incorrectly believe wills protect them from probate cour. This is false. A will must go through probate to be validated and executed. Only properly funded trusts avoid probate.

Myth #3: "Estate planning is only for older people"

Just 22% of Millennials have a will, and over 60% have no estate planning documents at all. Yet unexpected deaths, accidents, and illnesses can strike at any age—especially if you have minor children who need guardian designations.

Myth #4: "It's too expensive to set up a trust"

The cost of setting up a trust is typically a fraction of what probate will cost your estate. When you consider that probate expenses can eat up to 10% of an estate, proper planning is actually a significant money-saver.

The Nine Categories Checklist

To make this actionable, here's your complete checklist of what belongs in your trust:

✓ Real Property: Houses, land, commercial property, mineral rights

✓ Personal Property: Vehicles, jewelry, furniture, firearms, art, collectibles

✓ Intangible Property: Patents, copyrights, trademarks, websites, domain names

✓ Income & Financial Assets: Stocks, bonds, royalties, rental income, CDs, cash, HSAs

✓ Retirement Accounts: 401(k), IRA, pension plans (typically through beneficiary designation)

✓ Insurance & Annuities: Life insurance, annuities, long-term care policies

✓ Business Interests: LLC units, corporate shares, partnership interests, professional practices

✓ Digital Assets: Cryptocurrency, NFTs, online accounts, digital intellectual property

✓ Everything Else: If it has value and you want to control who receives it, put it in your trust

Take Action Today

The process of funding your trust might seem overwhelming, but it's far less complicated than leaving your family to navigate probate court without you.

Remember: Creating a trust is only the first step. The critical second step is funding it—actually transferring your assets into the trust's name. Michael Jackson had a trust, but because he failed to properly fund it, his estate still went through probate and remains entangled in legal disputes more than 15 years after his death.

Don't make the same mistake.

Your legacy deserves protection. Your family deserves the peace of mind that comes from knowing everything has been handled properly. And you deserve the confidence that your wishes will be carried out exactly as you intended—without government interference, public exposure, or unnecessary costs.

Need help? Apply for a 30 minute consultation here.

Disclaimer: This article provides educational information about estate planning and asset protection strategies. It is not legal, tax, or financial advice. Every situation is unique and requires personalized guidance from qualified professionals. Laws vary by state and change frequently. Consult with licensed attorneys, CPAs, and financial advisors before implementing any strategies discussed.

Recommended articles

Essential guides to protect and preserve your family's wealth

Stay informed about wealth protection

Get expert strategies and insights delivered to your inbox weekly