What Should You Put Into Your Trust? The Complete Asset Protection Checklist

The question haunts every estate planning consultation: "What exactly should I put into my trust?"

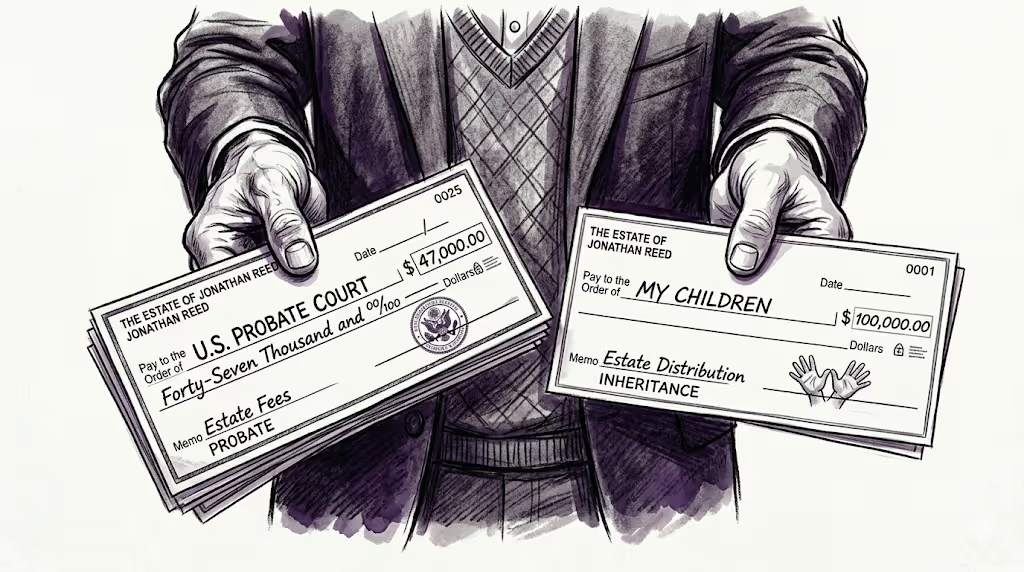

It's not theoretical. Last week, we spoke with an 80-year-old widow whose husband's failure to properly fund their trust cost their family $12,000 in probate fees—money that should have gone to their children instead of government processing.

The answer matters because according to AARP, 60% of American adults don't have a will or trust at all, and among those who do, a significant percentage have unfunded or incorrectly funded trusts that will ultimately fail their families when it matters most.

Why Trust Funding Matters More Than Having a Trust

Here's what most people misunderstand: having a trust document doesn't protect anything. It's the funding—the actual transfer of asset ownership into the trust—that provides protection.

Think of it this way: A trust is like a safe. You can own the best safe in the world, but if your valuables are sitting on the kitchen counter, the safe doesn't protect anything.

During your lifetime, when your trust is revocable, you maintain complete control. Want to sell your house? Go ahead—you still receive the capital gains benefits. Want to trade cryptocurrency held in the trust? You have full authority to do so. The revocable nature means the trust is essentially transparent for tax and control purposes.

But here's the crucial mechanism: Upon your death, the trust becomes irrevocable. This transformation is what protects assets from probate court, provides privacy, and enables controlled distribution according to your wishes rather than state intestacy laws.

The Probate Reality Nobody Discusses

Probate courts process thousands of cases every single day across America. According to the National Center for State Courts, probate cases represent a substantial portion of civil court proceedings, with the average probate case taking 6-24 months to resolve—sometimes longer for complex estates.

The costs are equally sobering. According to estate planning research, probate costs typically range from 5-10% of the estate's total value, including court fees, attorney fees, executor compensation, and appraisal costs. For a $500,000 estate, that's $25,000 to $50,000 that goes to fees instead of beneficiaries.

The Nine Categories of Assets That Belong in Your Trust

Let's break down exactly what needs trust protection, organized into nine comprehensive categories:

1. Real Property

Real property encompasses any land and permanent structures attached to it. This category includes:

- Primary residences and vacation homes

- Undeveloped land and agricultural property

- Mineral rights (including oil, gas, coal, and precious metals extraction rights)

- Commercial real estate (apartment complexes, office buildings, retail spaces)

- Timberland and water rights

- Easements and right-of-way agreements

Real-world example: We recently worked with a Kentucky landowner who owns 750 acres with coal mining rights. Without proper trust funding, his heirs would face not only probate delays but potential disputes over mineral extraction agreements worth hundreds of thousands annually.

Why it matters: Real property typically represents the largest portion of most estates. Probate proceedings for real estate require court approval for sales and can delay transactions for months, costing heirs market opportunities and ongoing maintenance expenses.

2. Personal Property

Personal property includes tangible items you can physically touch and move. This category covers:

- Vehicles (cars, trucks, motorcycles, boats, RVs)

- Jewelry and watches

- Furniture and household goods

- Firearms and weapon collections

- Art collections and antiques

- Musical instruments

- Safe deposit box contents

- Family heirlooms and memorabilia

The common misconception: "I'll just list these in my will, and my kids will split them up."

This fails because items not titled in the trust must pass through probate—even if your will specifies who gets what. The solution is bequeathing these items within your trust document, explicitly stating which items go to which beneficiaries.

Why it matters: Personal property often carries emotional value far exceeding monetary worth. Probate delays can force families to wait months or years to receive grandmother's wedding ring or father's watch collection. Worse, these items become public record during probate, potentially attracting unwanted attention.

3. Intangible Property

Intangible property holds value despite having no physical form:

- Patents and patent applications

- Copyrights and publishing rights

- Trademarks and service marks

- Website ownership and domain names

- Brand equity and goodwill

- Licensing agreements

- Franchise rights

The value test: If someone would pay money to own it, it needs trust protection.

Why it matters: In our digital economy, intangible assets often represent substantial value. A profitable website generating $10,000 monthly, a trademark used across multiple products, or patent rights generating licensing fees all require protection from probate exposure and proper succession planning.

4. Income-Producing Assets

This category covers assets that generate ongoing revenue:

- Stocks, bonds, and mutual funds

- Royalty payments (from books, music, inventions)

- Rental income from investment properties

- Insurance claim proceeds and settlement payments

- Certificates of Deposit (CDs)

- Cash holdings (in accounts or physical possession)

- Health Savings Accounts (HSAs)

- Flexible Spending Accounts (FSAs)

Important distinction: A rental property itself falls under real property, but the income stream it generates is a separate asset category requiring its own considerations.

Why it matters: Income-producing assets left outside trusts can create tax complications and force liquidations during probate to cover estate expenses, potentially selling during market downturns and destroying years of investment growth.

5. Retirement Accounts

Retirement accounts require special handling due to tax implications:

- 401(k) plans

- Traditional IRAs

- Roth IRAs

- 403(b) plans

- Pension plans

- Employee stock ownership plans (ESOPs)

- SEP IRAs and SIMPLE IRAs

Critical consideration: Unlike other assets, retirement accounts aren't typically retitled into your trust during your lifetime due to tax consequences. Instead, the trust is usually named as a beneficiary, with specific language ensuring tax-efficient distributions.

Why it matters: Improper retirement account handling can trigger massive tax bills. Without proper planning, beneficiaries might face immediate taxation on inherited traditional retirement accounts, potentially pushing them into higher tax brackets and losing decades of tax-deferred growth opportunity.

The urgency factor: Many people postpone retirement account planning because they're young and healthy. But unexpected death or incapacity doesn't wait for convenience. Without proper beneficiary designations and trust integration, families can spend months or years in probate court, watching retirement accounts they can't access while bills pile up.

6. Insurance Products and Annuities

Insurance and annuity products include:

- Life insurance policies (term and permanent)

- Policies with cash value accumulation

- Policy loan provisions

- Annuities (both qualified and non-qualified)

- Long-term care insurance with death benefits

- Disability policies with residual value

The beneficiary strategy: The most powerful approach is making your trust the beneficiary of life insurance policies rather than naming individuals directly.

Why this matters—A real scenario: Consider a $1 million life insurance policy payable to a 25-year-old child. Research on lottery winners and sudden wealth recipients shows that individuals without financial experience typically exhaust large sums within 1-2 years. According to a National Endowment for Financial Education study, 70% of people who receive a financial windfall lose it within a few years.

The spendthrift solution: When the trust is the beneficiary, you control distribution timing and amounts. Rather than a $1 million lump sum, you can structure monthly payments—perhaps $10,000 monthly—providing financial security without the destruction that often accompanies sudden wealth.

Conditional distributions—A real case study: We recently consulted with an 80-year-old client (we'll call her Lucy) whose adult daughter struggles with alcoholism. Lucy's daughter and son-in-law both suffer from alcohol addiction, and their children are growing up in that destructive environment.

Lucy didn't want to disinherit her daughter, but she also wouldn't enable her addiction. The solution: Her trust specifies that her daughter receives no inheritance until she maintains verifiable sobriety—monthly testing showing no alcohol use—for 24 consecutive months. After meeting this condition, distributions occur gradually over time.

This approach creates powerful incentive for recovery while protecting both the inheritance and the daughter's wellbeing. This is the customization power of properly structured trusts.

7. Business Interests

Business ownership takes many forms requiring trust protection:

- LLC membership units

- S-corporation stock

- C-corporation shares

- Partnership interests

- Professional practice ownership (medical, legal, accounting)

- Sole proprietorship assets

Why it matters: Business interests often represent decades of work and substantial value. Without trust planning, probate proceedings can force business sales during family transitions, destroy ongoing operations, or create disputes among surviving owners and heirs.

Operating freedom: Transferring business interests into your trust doesn't restrict your operational control during your lifetime. You continue managing, selling, or restructuring as needed. The trust simply ensures seamless transition without court interference when you're gone.

8. Digital Assets and Cryptocurrencies

Modern estates include substantial digital holdings:

- Cryptocurrency (Bitcoin, Ethereum, and altcoins)

- Cold wallet storage

- Hot wallet accounts

- Exchange account holdings

- NFTs (non-fungible tokens)

- Digital content libraries

- Cloud storage accounts

- Social media accounts with commercial value

Why it matters: Digital assets present unique challenges. Without proper trust funding and detailed instructions, cryptocurrency can become permanently inaccessible—literally lost forever if private keys aren't properly documented and transferred. The blockchain doesn't care about probate court orders.

The documentation imperative: Beyond titling digital assets to your trust, you need secure documentation of access credentials, private keys, and recovery phrases. This information must be accessible to your trustee but protected from theft or loss.

9. Special Considerations and Advanced Strategies

Beyond the eight primary categories, several special situations deserve attention:

Future inheritances: If you expect to inherit assets from parents or other family members, your trust can be structured to receive and manage those inheritances according to your estate plan rather than exposing them to probate.

Lawsuit proceeds: Personal injury settlements, judgment awards, and other legal recoveries should flow directly into your trust for protection.

Foreign assets: International property, foreign bank accounts, and overseas business interests require special planning due to multiple jurisdiction complications.

The Cost of Doing Nothing

Remember Lucy's husband—the story that opened this article? His estate paid $12,000 in probate fees because assets weren't properly titled. But the financial cost was actually the smallest loss.

The family endured:

- 18 months of probate proceedings before assets could be distributed

- Public court records exposing their financial details to anyone who cared to look

- Family stress and conflict during a time that should have been for grieving

- Lost opportunity costs as real estate markets shifted and investment accounts couldn't be managed

The Government Has a Plan for Your Estate

Here's the reality nobody wants to discuss: If you don't create a comprehensive estate plan with properly funded trusts, the government has created one for you. It's called intestacy law, and it:

- Requires probate court supervision (6-24 months minimum)

- Extracts fees of 5-10% of your estate value

- Makes all proceedings public record

- Distributes assets according to state formulas, not your wishes

- Creates opportunities for family conflict and litigation

Taking Action: Your Next Steps

Estate planning isn't something you do once and forget. It's an ongoing process requiring:

- Creation: Establishing your trust documents with proper legal guidance

- Funding: Titling all nine asset categories into your trust

- Updating: Reviewing and updating as life circumstances change

- Documentation: Maintaining clear records of digital assets and access information

- Communication: Ensuring your trustee and family understand your plans

The question isn't whether you need a trust—if you own any assets and care about your family's future, you do. The question is whether you'll take action before it's too late.

Because unlike the families sitting in probate court watching their inheritance get consumed by fees and delays, you still have time to protect what you've built.

Your loved ones will either remember you for the thoughtful planning that protected them during their grief, or they'll remember the six months they spent in court because you never got around to it.

Which legacy will you leave?

Need help? Apply for a 30 minute consultation here.

Disclaimer: This article provides educational information about estate planning and asset protection strategies. It is not legal, tax, or financial advice. Every situation is unique and requires personalized guidance from qualified professionals. Laws vary by state and change frequently. Consult with licensed attorneys, CPAs, and financial advisors before implementing any strategies discussed.

Recommended articles

Essential guides to protect and preserve your family's wealth

Stay informed about wealth protection

Get expert strategies and insights delivered to your inbox weekly